Rapid

diagnostic testing for influenza (RIDTs) are considered the gold standard for

diagnosing influenza. It is an immunoassay that can identify the presence of

influenza A and B influenza virus nucleoprotein antigens in respiratory

specimens and display the results in a qualitative manner (positive and

negative). Although RIDT is not as sensitive as other influenza detection

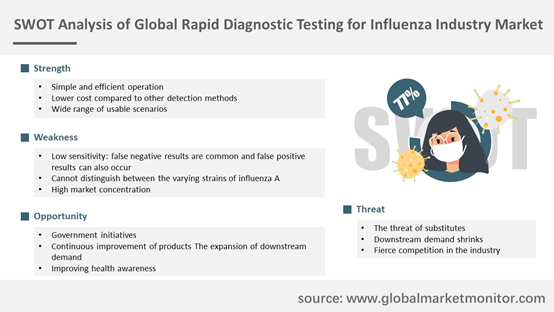

methods, this type of detection is simple to operate, with results within 15

minutes, and has the advantage of low cost. It is widely used in clinical

influenza diagnosis in clinical practice.

The

classification of RITD is based on influenza type. There are two types of

influenza A and influenza B. Both of these flus are seasonal flu, with similar

symptoms, coughing and fever. However, compared with type B influenza virus, type

A influenza virus is more likely to cause complications. Moreover, influenza A

virus is not only prevalent in humans, but also in livestock, as known as bird

flu, which can cause a large number of animal deaths. However, type B virus

influenza is generally a small-scale epidemic, and it does not infect animals

other than humans. It has a short infection period and usually recovers in

about a week. Influenza patients and invisible infected patients are the main

sources of infection, and they are generally prone to outbreaks during the

winter and spring seasons. Based on current data analysis, influenza B is more

common, with a market share of 54.90% in 2020.

The main application place of influenza rapid diagnostic test is hospital, which has the most complete medical facilities to provide the most complete services for patients who need flu testing. It can also be used for point-of-care testing, which refers to medical diagnostic tests performed at or near the point of care, that is, testing performed at the time and place of patient care.

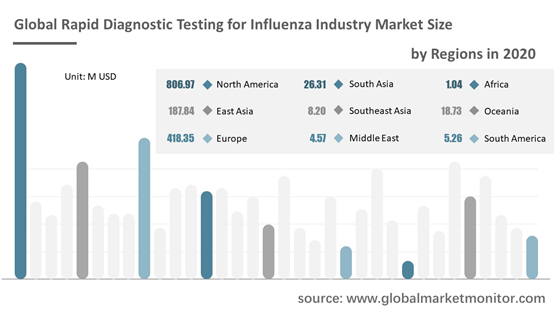

Analysis of Rapid Diagnostic Testing for Influenza Industry in Various Regions

North America is the largest revenue market with a market share of 56.42% in 2015 and 55.74% in 2020, a decrease of 0.68%. Europe ranked second with a market share of 29.03% in 2019. In addition, with the economic development, downstream demand increase and technological innovation and advancement of emerging economies such as China, India, and Brazil, have led to an increase in demand. It is expected that the Asia-Pacific, Middle East and Africa market will become the fastest growing market for rapid diagnostic testing for influenza industry.

Get the Complete Sample, Please Click: https://www.globalmarketmonitor.com/reports/763157-rapid-diagnostic-testing-for-influenza-market-report.html

Therefore, rapid diagnostic testing for influenza companies are mainly from North America, with relatively high industry concentration. The top three companies are BD, Abbott and Quidel, with revenue market shares of 24.71%, 24.08% and 13.12% in 2019, respectively.

The new crown epidemic has a strong destructive force and a long duration, which has severely affected the livelihood, economy, and politics of all countries in the world. However, after the epidemic, people have paid more and more attention to influenza testing, which has brought a new period of development opportunities for rapid influenza diagnostic testing. The revenue of this industry in 2020 has increase to 35.77%.

The Frequent Occurrence of Influenza Has Attracted the Attention of the Public, and the Demand for Rapid Diagnostic Testing for Influenza is Increasing

According to our research, the total sales of the global rapid diagnostic testing for influenza market in 2015 was US$798.25 million, which will increase to US$1447.67 million by 2020. The prevalence of influenza and the number of potential patients continue to increase, so public safety awareness has increased. It is expected that the global rapid diagnostic testing for influenza market will experience rapid growth during the forecast period. We predict that by 2026 the value of the rapid diagnostic testing for influenza market can reach 2393.69 million US dollars. The compound annual growth rate of rapid diagnostic testing for influenza from 2020 to 2026 is 8.74%.

Influenza is an important cause of human morbidity and death. High-risk groups include pregnant women, children, the elderly, immunosuppressed patients with chronic diseases, and medical staff. Although influenza is easy to treat, timely diagnosis and proper treatment are the key to eradicating the epidemic globally and play a vital role. But at present, rapid diagnostic kits are generally concentrated in general hospitals and pharmaceutical companies, and ordinary people rarely stock such flu essentials at home. However, as the awareness of influenza in developing countries and developed regions continues to increase, especially in the context of the COVID-19 epidemic, people are paying more and more attention to personal health. Due to the advantages of quick results, simple use, and not requiring much professional knowledge other than basic operating knowledge, rapid diagnostic testing for influenza will become more common in the home or office of the general public in the future.

Most

people infected with the flu are mildly ill, do not require medical care or

antiviral drugs, and will recover within two weeks. However, some people are

more likely to suffer from flu complications, leading to hospitalization and

sometimes death. Pneumonia, bronchitis, sinus infections, and ear infections

are examples of flu-related complications. Influenza can also worsen chronic

health problems. According to data from the Centers for Disease Control and

Prevention, certain high-risk groups may experience severe flu-related

complications if they contract the flu. The number of influenza patients

remains high, and the susceptible population is increasing. The population of

65 years and over grows faster than all other age groups, which promotes the demand

for influenza prevention and treatment. Among them, how to quickly determine

whether you have flu is also an important link, which means that the demand for

rapid flu diagnostic testing will gradually increase.

The

industry can adopt a variety of distribution strategies to form economies of

scale through upstream and downstream integration and horizontal competitor

alliances to expand market share, which is conducive to entering the target

market, sharing the cost of developing new products, and improving its own

bargaining power for upstream and downstream.

We provide more professional and intelligent market reports to complement your business decisions.

Chinese

Chinese