Historically, the first agent used for embolotherapy was autologous blood clot. This was easily and quickly obtained and was inherently biocompatible. The drawback of autologous blood clot is that as the body\'s natural clot lysis dramatically limits the durability of occlusion; recanalization can recur within hours to days. The next agents developed were fascial strips harvested from dura and tensor fascia lata. Silk threads were also historically used as embolic agents, notably for intracranial vascular malformations. Today with the advent of modern liquid and particulates, silk, clot, and fascia are not used.

Modern embolic agents are either temporary or permanent. Permanent agents are more common, and there are many applicable subsets including liquid agents, particulates and coils.

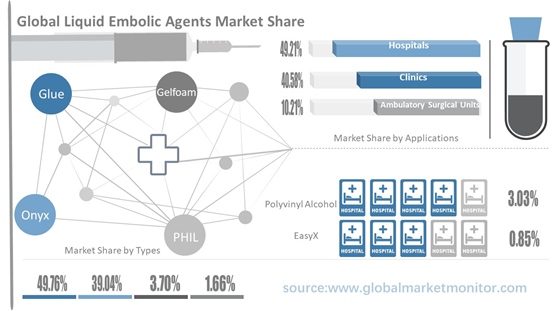

Liquid embolic agents include gelatin foam, which is a biologic substance made from purified skin gelatin. The temporary nature of gelatin foam occlusion can be either an advantage or disadvantage depending on the clinical situation. Advantages of Polyvinyl Alcohol (Squid) include that it is non-adhesive. This allows for longer injection times and the ability to temporarily suspend embolization and proceed with further angiography mid procedure if necessary. Precipitating hydrophobic injectable liquid, a novel iodinated copolymer based liquid embolic agent, PHIL is feasible for transarterial embolization in an acute and subacute endovascular embolization model. Onyx is a non-adhesive liquid embolic agent comprised of EVOH (ethylene vinyl alcohol) copolymer dissolved in DMSO (dimethyl sulfoxide), and suspended micronized tantalum powder to provide contrast for visualization under fluoroscopy. Liquid embolic agents also include glue and EasyX, the EasyX liquid embolic is a new injectable, precipitating polymeric agent for the obliteration of vascular spaces through direct puncture or catheter access performed under X-ray guidance. In 2017, different types covered a market share of 3.70%,1.66%,3.03%,49.76%,39.04% and 0.85%.

Liquid embolic agents are used in the treatment of bleeding in the operating room, oncology treatment of tumors, vascular lesions and tumor embolization in hospitals. Liquid embolic agents are used in clinics to treat chronic tumors and vascular lesions. Liquid embolic agents are used in ambulatory surgical units to interrupt the blood supply during surgery and achieve hemorrhage control. In 2017, these three application fields respectively covered a market share of 49.21%,40.58% and 10.21%.

The Current Situation of Liquid Embolic Agents Industry Market

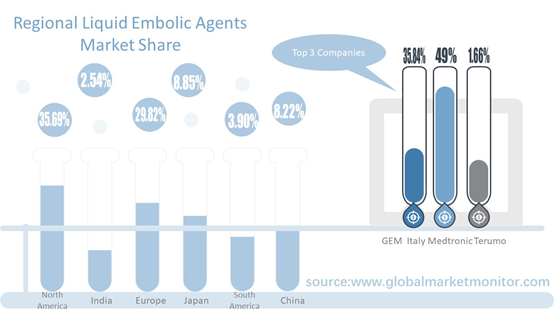

Liquid embolic agents companies are mainly from United States and Europe; the industry concentrate rate is very high. The top 3 companies accounted for more than 92.97%, they are Medtronic,GEM Italy and Terumo, respectively covered a market share of 55.47%,35.84% and 1.66%.

North America was the largest revenue market with a market share of 36.23% in 2013 and 35.47% in 2018 with an increase of -0.76%. Europe ranked the second market with the market share of 29.82% in 2017. Also, emerging markets for liquid embolic agents are expected to be the market with the most promising growth rate. Development of economy, rising per capita income of people, more and more downstream demand has led to an increase of this industry.

The growth of the liquid embolic agents market is largely driven by downstream consumptions. Some of the major factors, such as improvement of health and medical awareness among residents, the improvement of economic income, increase of people suffering from cancer and chronic diseases, many local businesses emerged to the market, which boost the market growth.

Get the complete sample, please click: https://www.globalmarketmonitor.com/reports/762940-liquid-embolic-agents-market-report.html

Liquid Embolic Agents Industry Market Forecast

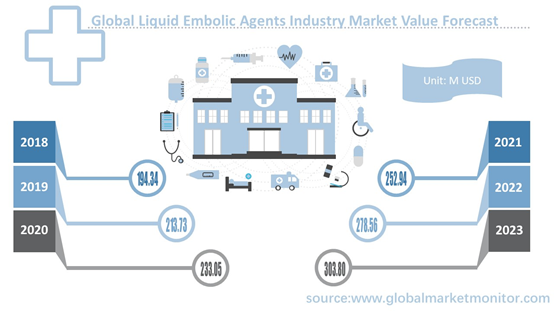

According to our research, the global liquid embolic agents market has a total sales value of 121.34 M USD back in 2013, and increased to 194.34 M USD in 2018. We made a series of functional calculation and deduced the past 5 year’s data with scientific model. Finally, we made the prediction that the value of liquid embolic agents markets can be 303.80 M USD by 2023.The CAGR of liquid embolic agents is 9.49% from 2017 to 2023. North America will remain its first place with a market share of 103.20M USD and as the second largest market, Europe will reach a market share of 84.30M USD.

The raw materials of medical liquid embolic agents mainly are graphene. This kind of embolic agent has simple composition, and is convenient store and easy to realize mass production. It is simple to operate and non-sticky tube, which can avoid vascular damage and bleeding during surgery to the greatest extent, and is expected to provide better treatment options for patients with various cerebrovascular diseases.

Graphene is a two-dimensional carbon nanomaterial with a honeycomb lattice composed of carbon atoms. It is the thinnest, strongest, and strongest new type of material that has been discovered so far. These characteristics determine that graphene is the material with the lowest electrical resistivity has better thermal conductivity than any metal. Graphene has great potential in applications such as new energy vehicles.

Since the signing of the Paris Agreement, countries around the world have actively responded to the UN’s call for “carbon neutrality”, and China has set a carbon neutral goal by 2060. To achieve carbon neutrality, it is necessary to accelerate the replacement of old and new energy sources and develop new energy sources to replace traditional high-carbon emission coal resources. The replacement of fuel vehicles by new energy vehicles is an important carbon emission reduction measure for the transportation industry. The demand for graphene, an important raw material for new energy vehicle batteries, will also greatly increase, and the entire graphene industry will develop rapidly. The growth of raw materials in the upstream market and the downstream consumer market will promote the stable development of the overall liquid embolism industry.

On the flipside, unfavorable reimbursement scenario, stringent government regulations, economic trade protection and fluctuation of the price of raw materials may hinder the market growth. In the future, the manufacturers tend to increase research and development efforts, apply for certification in different regions, improve its productivity and create competitive advantage, such as offering more high performance product at a cost-effective price point.

Get the complete sample, please click: https://www.globalmarketmonitor.com/reports/762940-liquid-embolic-agents-market-report.html

We provide more professional and intelligent market reports to complement your business decisions.

Chinese

Chinese