Pearlescent materials originated from the preparation of pearlescent powder from natural shells and were used in noble and royal decorations in the early days. In the 1960s, DuPont invented a method of producing pearlescent materials coated with titanium oxide sulfate using mica as a substrate, which has started the industrialization of pearlescent materials. Since then, the technology of pearlescent materials has been continuously developed around the world, and a relatively complete technology process of pearlescent materials have been formed, widely used in coatings, plastics, automobiles, cosmetics, inks, leather, ceramics, and building materials.

Enquire before purchasing this report-

https://www.globalmarketmonitor.com/request.php?type=3&rid=591673

Synthetic Mica Becomes the First Choice

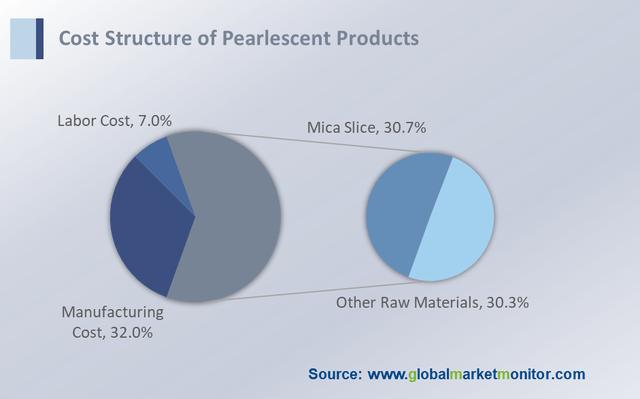

Mica material is the main raw material of pearlescent materials, accounting for about 30% of the raw material cost. Other materials include metal oxides such as titanium dioxide and iron trioxide for coating. The raw materials account for more than 60% of the entire production cost of pearlescent materials.

Early natural pearlescent materials contained natural pearl ingredients, which were silver-white organic crystals derived from fish scales or fish skin. It has gradually been replaced by synthetic pearlescent materials due to the limited source of natural substance, high production cost, and poor stability.

The artificially synthesized pearlescent materials mainly include mica-based pearlescent materials, bismuth oxychloride crystal pearlescent materials, and lead carbonate crystal pearlescent materials. Since bismuth oxychloride crystals have poor optical stability and durability and lead carbonate crystals are highly toxic, the pearlescent materials currently on the market mainly use non-toxic and easily available natural mica as the basic material. Mica-based pearlescent material is currently the most produced and most widely used pearlescent material in the world.

The Domestic Pearlescent Material Industry Is Supported by National Policies, And the Market Scale Continues to Expand

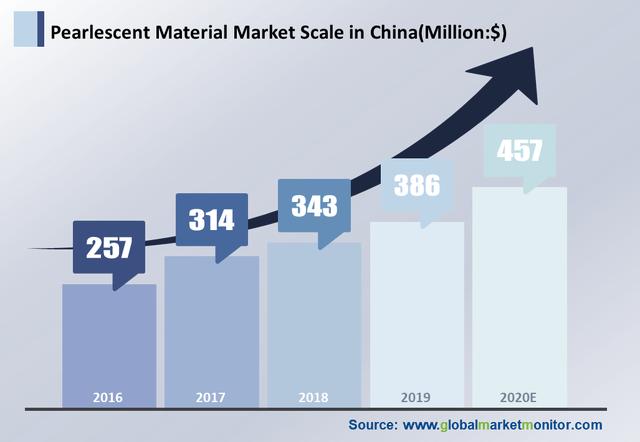

Pearlescent material, based on the high-tech, is one of the most potential industries in the 21st century along with information technology and biotechnology, which is listed as the development focus in the field of New pigments and dyes. The encouraging policies give guidance for the pearlescent material industry, which contributes to the rapid increase and a competitive atmosphere to form. With the dramatic increase of the domestic economy, the market scale of the pearlescent material rises greatly, from 257 million US dollars in 2016 to 386 million US dollars in 2019, which is expected to be 457 million US dollars in 2020.

Increasing Competition in the Low-End Market

Due to the small scale of most domestic pearlescent material production enterprises, low product quality, limited marketing capabilities, and serious product homogeneity, most of them rely on a low price to compete for market share, causing the chaotic situation of excess product and price reduction with each other. Increasing competition in the low-end market is not conducive to technological innovation in the industry. In the future, with the increase in industry integration and concentration, it will be conducive to the implementation of technological innovation in the high-end field, cultivating industry leaders to comprehensively promote the development of the industry, in line with the long-term development of the pearlescent materials industry.

The Status of the Pearlescent Material Market

The top three companies in the global market of pearlescent materials are Merck in German, BASF, and Fujian Kuncai, in which Merck mainly produces optical raw materials, BASF involves in many fields, and Fujian Kuncai is the only company that specializes in the production of pearlescent materials among the top three, and is also the only company that can mass-produce synthetic mica.

Fujian Kuncai currently has an annual output of 30,000 tons of pearlescent materials, occupying 10-15% of the global market share, as the world's largest pearlescent material manufacturer. At present, there are more than 20 peer companies competing in China, most of which are fierce competition of low-end products of pearl materials, while Kuncai is positioned as high-end products in the industry. Because of the core technologies that Kuncai has, it is difficult to shake its leading position in the short-medium term in the domestic pearlescent material industry.

From the perspective of demand, pearlescent powder has achieved localization in traditional industrial applications. There are more than 20 pearlescent powder manufacturers in China, in which the industry leader has maintained a gross profit margin of more than 40% for many years. In terms of high-end applications, Merck, BASF, and CQV rank in the top three, among which Merck dominates the global automotive-grade pearlescent powder market with a market share of more than 60% and a product gross margin of more than 70%. Due to the huge profits, many domestic companies have tried to enter, but only Kuncai Technology has been recognized by the industry and has increased its volume significantly.

Hidden Industry Champions Break Through Numerous Technologies and Are Expected to Subvert the Industry Pattern

Kuncai's core competitiveness lies in innovation, whose years of deep cultivation have enabled the company to establish strong technical barriers and continue to benefit from the dividends of technological innovation.

First, Kuncai broke through the core technology of surface treatment and synthetic mica, breaking the global market barriers for high-end pearlescent materials, in which key barriers of high-end pearlescent materials are surface treatment technology and heavy metal content. Second, Kuncai adopts the world's first self-developed technological method for preparing titanium oxychloride and ferric chloride by extraction method, replacing the two main raw materials, titanium tetrachloride and ferric chloride, previously relied on outsourcing. The self-developed new technology has many merits to ensure raw materials supply, greatly reduce costs, and improve product quality. The former titanium oxychloride production line has entered stable production, which is certainly estimated that the decline in manufacturing costs in 2020 is a definite trend. Third, Kuncai superimposes the leading technology of titanium dioxide and iron oxide surface coating to take the leading position in the high-end market of titanium dioxide and iron oxide Advantage, which is expected to reshape the market structure of titanium dioxide and iron oxide and become a leader in new technologies in the industry.

Although the pearlescent pigment industry in China is mainly concentrated in the low-end and middle-end areas, the international competitiveness of domestic enterprises will also continue to expand because domestic companies have greater advantages in terms of price and delivery cycle, as well as the technology progress toward automation, refinement, and high-end in the future.

LEARN MORE:

Pearlescent Pigment

https://www.globalmarketmonitor.com/reports/591673-pearlescent-pigments-market-report.html

Custom Reporting

https://www.globalmarketmonitor.com/request.php?type=9&rid=0

We provide more professional and intelligent market reports to complement your business decisions.

Chinese

Chinese