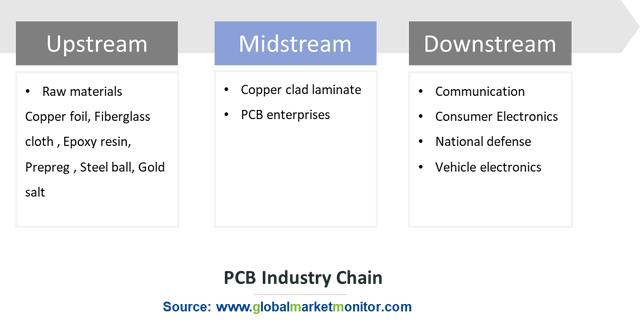

PCB Industry Chain

Each part of the PCB industry chain is divided, including upstream raw materials, midstream substrates, and downstream applications.

Enquire before purchasing this report-

https://www.globalmarketmonitor.com/request.php?type=3&rid=589246

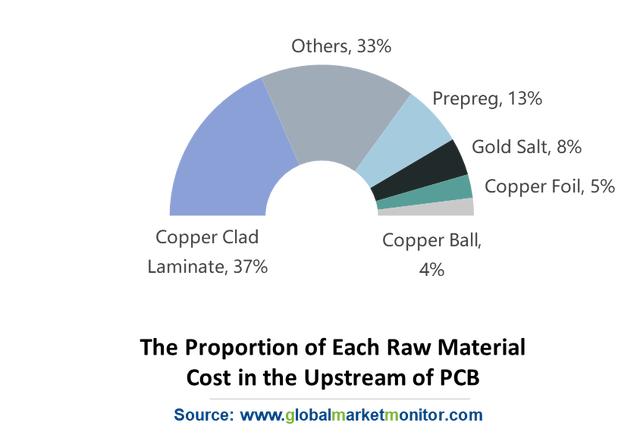

The proportion of raw material costs in PCB operating costs is relatively high, about 60-70%. Therefore, the raw materials have a great impact on the overall PCB industry. Copper foil, copper balls, copper foil substrates, prepregs, gold salts are the main raw materials required for PCB production.

In various raw materials, the proportion of the copper-clad laminate cost is the biggest, accounting for about 40%, which plays a significant role in the PCB industry, followed by prepreg, gold salt, and copper foil.

Copper-clad Laminate is an Important Material for PCB

Copper-clad laminate is a plate material made of wood pulp paper or fiberglass cloth as a reinforcing material, and is impregnated with resin glue and covered with copper foil on one or both sides through a hot press.

Copper-clad laminate is the core substrate of PCB manufacturing, accounting for about 30%-40% of the cost of PCB materials. And copper foil, resin, and glass fiber cloth are the major raw materials for copper-clad laminates, all of which contribute to the function of conduction, insulation, and support respectively. In CCL, copper foil accounts for 30% of the CCL thick plate cost and 50% of the thin plate; glass fiber cloth accounts for 40% of the CCL thick plate cost and 25% of the thin plate; epoxy resin accounts for about 15%.

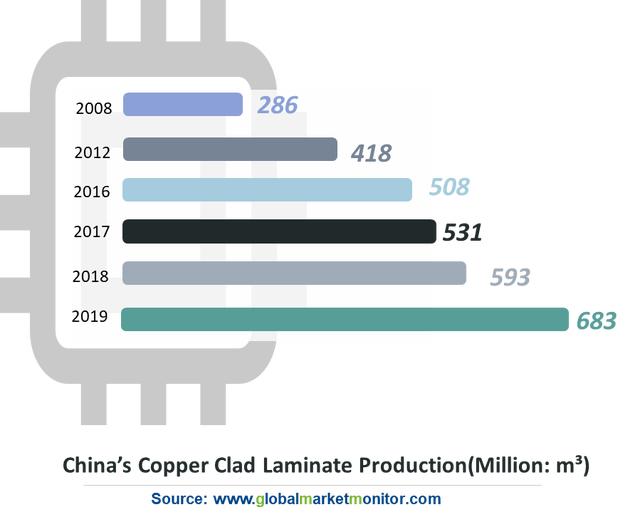

In 2019, the overall output of China's copper-clad laminate industry was 683 million cubic meters, a year-on-year increase of 15.4%.

The output of rigid copper-clad laminates in mainland China has not changed much, mainly including fiberglass cloth substrates, paper substrates, composite substrates, and metal substrates. Among them, the proportion of composite substrate CEM-1 and metal substrate copper-clad laminates has increased; glass fiber cloth substrate copper-clad laminates still account for the highest proportion of copper-clad laminate production in mainland China, accounting for 60.72% of the total output of copper-clad laminates, and the output reached 341 million cubic meters.

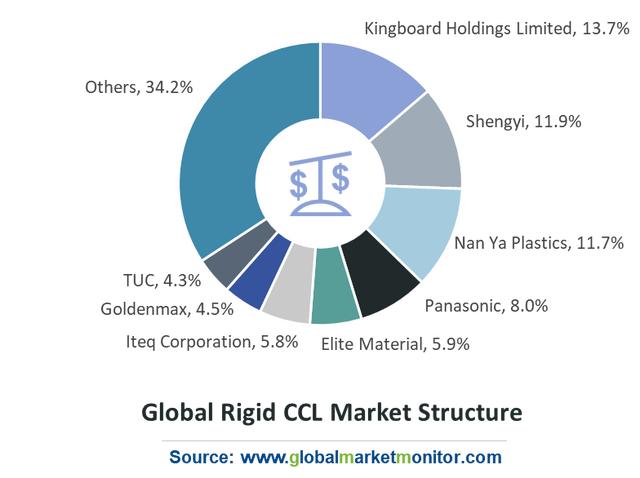

Copper-clad Laminates Industry Has A High Concentration, With A Stable Competitive Landscape

The copper-clad laminate industry is highly concentrated in which the scale of the company is relatively large. The global copper-clad laminate industry has formed a relatively concentrated and stable pattern. The scale of investment in fixed assets of copper-clad laminate companies is relatively large, which can be seen from that the price of a press is more than 12 million yuan. The construction of a complete production line requires a large-scale capital investment. Besides, with the acceleration of product upgrading and quality standards and the improvement of environmental protection and safety standards, enterprises will gradually increase their investment in production process equipment, safety and environmental protection equipment, research and development facilities, and personnel reserves. Secondly, companies in the industry have stable downstream customers, which is a barrier for the new entrants. Under normal circumstances, customers will not easily change suppliers.

The top ten copper-clad laminate manufacturers account for 74% of the market, in which the top three companies with the largest output value are Kingboard Group, Shengyi Technology, and Nan Ya Plastics. The output value of the above three companies accounts for more than 37% of the global share of the global copper-clad laminate. The industry has formed a relatively concentrated and stable pattern.

The Importance of Copper Foil in PCB Materials

Copper foil is made by copper and another mental in a certain percentage, which is deposited on a thin, continuous metal foil on the base layer of the circuit board, as a conductor to conduct electricity and dissipate heat. Single-sided or double-sided PCB boards cannot use copper foil and only use copper-clad laminate as the substrate. Copper foil is only used for the production of 4-layer and above multi-layer boards. Each multi-layer board only needs two pieces of copper foil. The amount of copper foil has nothing to do with the number of layers. Copper foil usually uses micrometers to express its thickness. The thinner and wider the copper foil is, the more difficult it is to produce.

Electronic copper foil can be divided into rolled copper foil and electrolytic copper foil according to the manufacturing process. Compared with electrolytic copper foil, the rolled copper foil process is more complicated and the production cost is higher.

At present, more than 90% of the world's copper foil is electrolytic copper foil. The price of copper foil mainly depends on the price change of copper, which is greatly affected by the international copper price. The international copper price has fluctuated in the past ten years. From 2016 to 2017, affected by the policy and supply-demand relationship, the copper price climbed from a trough to a peak.

The Domestic Electronic Copper Foil Sub-Industry Has A Layout, And the Industry Structure Is Expected to Be Further Optimized

In 2019, the demand for China's standard copper used in the CCL and PCB is 300,000 tons; the production capacity of copper foil for CCL and PCB is 346,500 tons, which can be seen that the supply exceeds demand. Besides, the demand for lithium battery copper foil used in the battery lights is about 138,400 tons, and its production capacity reached 235,900 tons, in which the supply is significantly greater than the demand. We predict that in 2020, the supply of China's electronic copper foil market will significantly exceed the demand, especially the lithium battery copper market. In the next few years, the low-level, homogeneous product market competition in the electronic copper foil industry will become more intense.

There are more prominent companies in the subdivision of the domestic electronic copper foil industry. Among them, the lithium battery copper foil companies mainly include Nord shares, Jiayuan Technology, Anhui Tongguan, in which the shipments of the top five lithium batteries accounted for 72% of the total lithium battery copper foil shipments. In the field of standard copper foil, there are mainly Kingboard Group, Changchun Chemical, Nan Ya Copper Foil, Anhui Copper Crown. The current lithium battery copper foil market is still in the growth stage, which is the main driving force for the development of electrolytic copper foil in the future.

LEARN MORE:

PCB

https://www.globalmarketmonitor.com/reports/589246-printed-circuit-board-pcb--market-report.html

Custom Reporting

https://www.globalmarketmonitor.com/request.php?type=9&rid=0

We provide more professional and intelligent market reports to complement your business decisions.

Chinese

Chinese