Medical devices refer to instruments, equipment, and appliances, and in vitro diagnostic reagents, and other similar or related items used directly or indirectly on the human body, including the required computer software. The utility is mainly obtained through physical methods, not through pharmacology, immunology or metabolism.

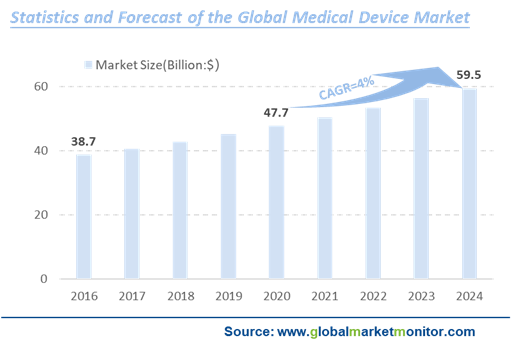

The Global Medical Device Market Continues to Grow

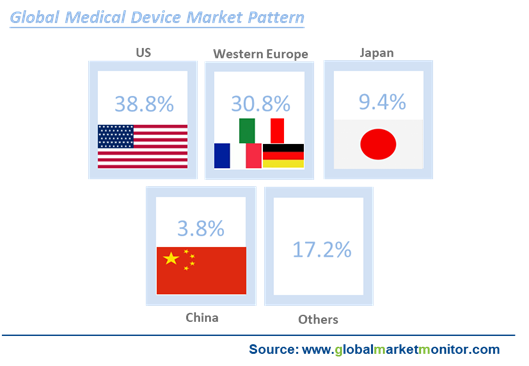

In terms of the distribution of the global medical device market, the medical device industry in developed countries and regions such as Europe and the United States started early. The income level and living standards of residents are relatively high, and the quality and service requirements of medical device products are relatively high, with a huge demand and stable growth.

In 2017, the global medical device market has exceeded the 400 billion US dollar. In 2019, the global medical device market was US$451.9 billion, which is expected to reach 477.4 billion US dollar in 2020.

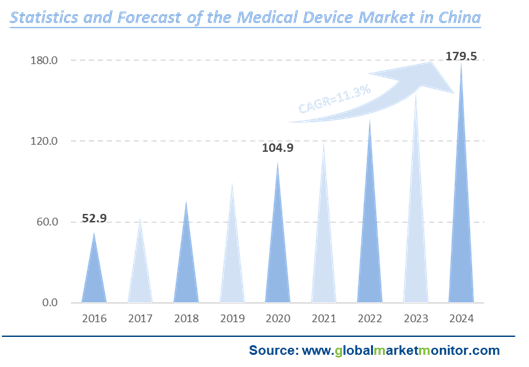

Medical Device Market in China Is Promising

With the increase in national disposable income and medical demand brought about by the aging of the population, and the improvement in the coverage, and depth of medical insurance, the demand for medical devices in China will continue to increase. At the same time, the policies have been taken to encourage medical device innovation and technological upgrading and open up a convenient channel for domestically-made innovative medical devices, and promote import substitution, which can been seen that the demand side and policy side jointly promote the rapid development of the domestic medical device market.

From 2014 to 2019, domestic medical device market maintained a rapid growth trend, from 370 billion yuan in 2016 increasing to 628.5 billion yuan in 2019. It is estimated that the market size of the medical device industry will exceed 1.2 trillion yuan in 2024 and the next ten years will be the golden period for the development of medical device industry of China, with a CAGR of above 10%.

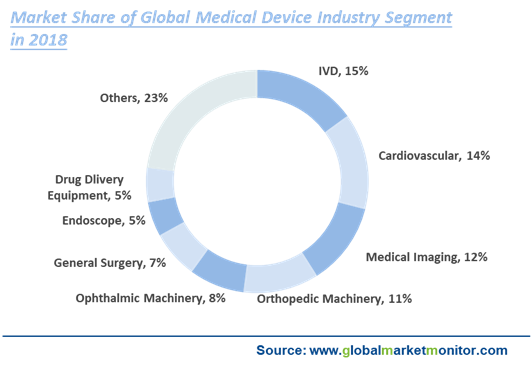

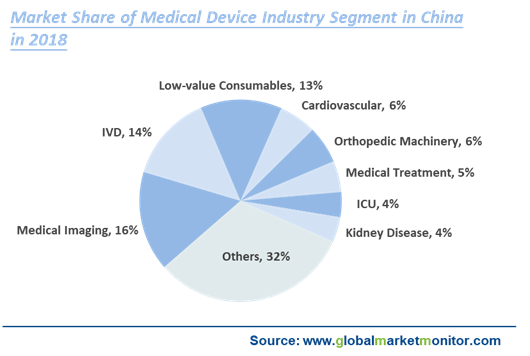

IVD Is the Largest Sub-Sector of Medical Devices in the World, While in China It Is Medical Imaging

From the perspective of the global medical device segmentation, IVD is the largest sub-sector of the global medical device industry, accounting for 15% of the total market, followed by cardiovascular-related devices accounting for 14%, and medical imaging devices rank third. In China, imaging, IVD, and low-value consumables occupy the top three places. Medical imaging is the segment with the largest share, accounting for 16%.

There Is A Shortage of Domestic Medical Infrastructure, Which Will Be Quickly Filled After the Epidemic

There is a shortage of medical infrastructure in China, and the construction of hospitals will be accelerated after the epidemic. As the number of 3A grade hospitals in a city fully shows the local medical resources and level, Wuhan which is the fourth city in the country in terms of the number of 3A grade hospitals still has the shortage of medical resources, which reflects the fact of the real medical level in China and is actually a wake-up call to most cities in China that medical resources need to be strengthened. According to incomplete statistics, 6 regions have already proposed hospital construction plans. Suzhou City announced that during the "14th Five-Year Plan" period, the number of tertiary hospitals will increase by 50% to 36, and the number of tertiary hospitals will strive to increase by 10 Family.

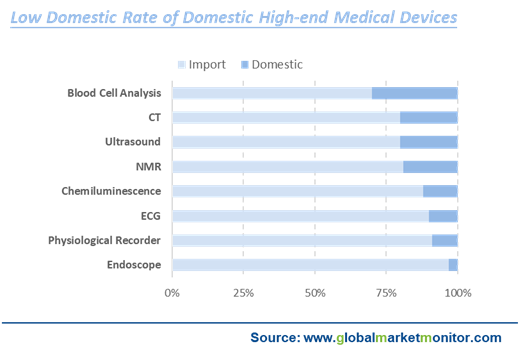

The Domestic High-End Medical Equipment Domestic Rate Is Low with Broad Import Substitution Space

Although the domestic imaging industry has achieved rapid development in recent years, the high-end imaging market especially in the fields of CT, NMR, and endoscopy is occupied by foreign capital with 80% of the market share, and local medical imaging companies occupy a place in the middle and low-end markets, limited by the gap in technology, brand, and comprehensive product performance. On the whole, the medical equipment in China is still dominated by low-end and mid-range products, with a lot of room for product structure upgrades. If breakthroughs can be made in the high-end field, the prospect of import substitution is broad.

In response to the low localization rate of high-end medical equipment, General Secretary Xi Jinping requested that high-end equipment be accelerated independently and controllable. It is expected to strengthen the construction of intensive care units after the epidemic. And the state issued that it is necessary to settle the shortcomings of high-end medical equipment, accelerate the research on key core technologies, and realize the independent control of high-end medical equipment, which sets the tone for the development of domestic high-end equipment.

Domestic Medical Equipment Leaders Are Far Behind International Leaders

Among the domestic 59 listed companies that have disclosed their annual reports, it is generated a total operating income of 108 billion yuan, a year-on-year increase of 13.98%, and created a net profit of 15.774 billion yuan, a year-on-year increase of 10.57%, in which Shenzhen Mindray ranked first with 16.556 billion yuan, a year-on-year increase of 83.39%,

However, the total revenue of the top 10 medical device companies in 2019 was 61.27 billion yuan, which is far less than the revenue of 211.1 billion yuan of Medtronic, the global medical device leader. It can be seen that there is a big gap between domestic leading enterprises and international leaders, with huge room for development.

At the same time, the revenue gap of the 59 listed companies in 2019 is relatively large. The top 20 listed companies have the highest revenue of Mindray Medical, with revenue reaching 16.556 billion yuan, and that with the lowest revenue is Shenzhen Glory, with 1.531 billion yuan. The revenue growth rate of Top20 listed companies' revenue year-on-year is generally at a relatively high level.

Generally speaking, the level of medical equipment in China has developed rapidly, but there are still shortcomings in terms of technical level, industrial scale, and layout of key subdivisions compared with the international level. As China’s economy maintains high-quality development, national income continues to increase, and medical insurance coverage and depth increase, medical coverage will become greatly wider and more medical needs will be brought by the aging of the domestic population. Thus, demand for medical devices in China is stronger than other countries.

Custom Reporting

https://www.globalmarketmonitor.com/request.php?type=9&rid=0

We provide more professional and intelligent market reports to complement your business decisions.

Chinese

Chinese