Since 2011, the auto market in first-and second-tier cities has approached saturation. Coupled with the restrictions on license plates and purchases there, it is difficult to increase for promotion in the auto market. Data show that in 2018, the auto market in China showed the first decline after years of growth. In 2019, auto production and sales continued to decline.

Compared with first- and second-tier cities, the potential of car consumption in third-tier cities and above is becoming more prominent. The sinking market has a low degree of exploitation, with a strong demand waiting to be released. Therefore, sinking the market has become the key development direction of the automotive industry in the future.

However, it is worth noting that although the lives of residents in the sinking market have greatly improved, their income levels are still in the not high stage. Residents in the sinking market have relatively few consumer choices, so they are more sensitive to commodity prices. While automobiles have gradually become a necessity in people's daily lives, the willingness of the sinking market groups to purchase automobiles also remains high. In this context, the auto financing leasing model is booming.

About Auto Finance Lease

Automobile financing lease based on cash installments introduces the characteristics of separation of ownership and use rights in rental services, and transfers ownership to the lessee after the lease ends. The business of automobile financing leasing is divided into two models of sale and leaseback and direct leasing.

The sale and leaseback is that a customer who already owns a car and want to obtain funds at one time, mortgages the car to a financial leasing company, and then the financial leasing company leases the car to third-party consumers who have the right to use the vehicle. When the agreement expires, the customer can get the ownership of the vehicle by paying the balance or disposes of the vehicle in the agreed manner.

Direct leasing refers to consumers who are interested in a certain car, and the leasing company buys the car in full and leases it to consumers. Consumers need to pay a certain deposit and pay the rent in installments. During the lease period, the ownership of the car belongs to the leasing company and the right to use belongs to the consumer. After the lease expires, the customer can choose to pay the balance to obtain the ownership of the vehicle or allow the leasing company to take the vehicle back. In this way, customers can drive in the car without having to bear too much financial pressure.

At first, in addition to buying cars in full, consumers mainly bought cars through bank car credit models. The industry regards auto finance leasing as the new vitality of the auto consumer market because auto finance leasing is superior to consumer credit in terms of accessibility standards and flexibility.

From the perspective of the results, both auto financing lease and bank auto credit obtain cars through installments, which can alleviate the relationship between capital and demand, but in actual operation, there are many differences between the two, mainly in the down payment amount, ownership relationship, and handling procedures.

In terms of down payment line, the down payment ratio of auto credit is generally between 20%-50%, and that of auto financing lease is generally less than 10%; in terms of ownership, consumers who buy cars through bank loans own the ownership of the vehicle. In the financial leasing model, the financial leasing company owns the ownership of the vehicle during the effective period of the financial leasing contract; in terms of procedures, due to the higher credit requirements of the lender for auto credit, the processing procedures of bank auto credit are more complicated. While the auto financing leasing company owns the ownership of the vehicle, the creditworthiness requirements of the lender are relatively low, with the relatively simple handling process.

The Development of Domestic Automobile Financial Leasing Is Still in the Early Stage

Auto finance leasing originated in the United States, whose development in developed countries such as Europe and the United States with a relatively high penetration rate is relatively mature. In 2018, the penetration rates of auto finance leasing in the United States, Germany, and France were 32%, 21.3%, and 18.5% respectively. In China, the development of automobile financial leasing is still in the early stage, with a market penetration rate of only 4.4%, which has great growth potential.

In the early days, domestic auto finance was dominated by consumer credit and auto insurance, in a relatively simple form, and experienced ups and downs in supervision. The rise of auto financing in recent years has benefited from the establishment of laws and regulations, the diversified market demand for auto finance, and the development of the Internet.

The Demand for Cars in the Sinking Market Is Gradually Released, With Great Market Potential

Related surveys show that 46.83% of the respondents in the sinking market said they plan to buy cars in the next year, and 70% of them have the need to exchange and purchase more vehicles.

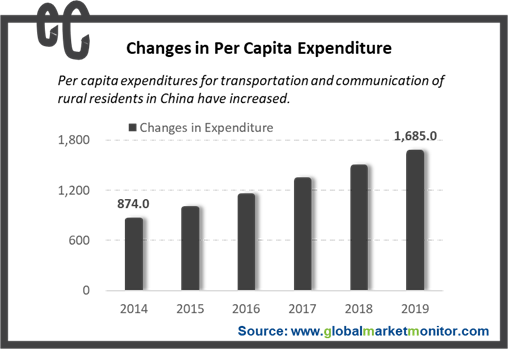

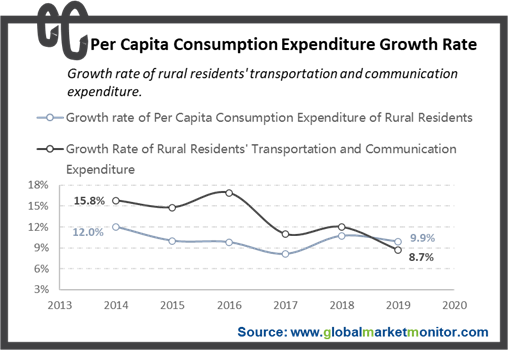

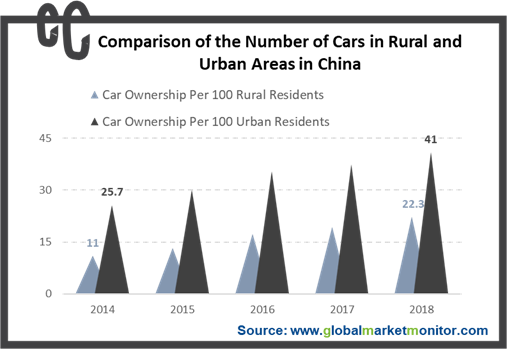

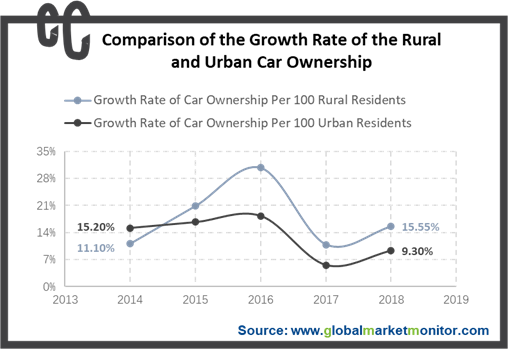

The rural population of China is large. With the continuous increase of rural per capita disposable income, the rural population's demand for automobiles and purchasing power are gradually increasing.

Since most of the rural population does not have stable jobs and good credit certificates, it is difficult to apply from the bank. And a one-time payment for a car will bring short-term financial pressure. The low threshold and low payment ratio of automobile financing leasing products are more suitable for the consumption characteristics of rural residents than bank car loans. Therefore, how to release the consumption power of the sinking market is the key to the recovery of the auto market.

There Are Many Problems and Risks in the Domestic Automobile Financing Leasing Industry

From the consumer perspective, the primary problem is high rates. In the domestic market, the rate of the "1+3" program is generally above 20%, while this rate is less than 10% in the mature market. Although car financial leasing provides a flexible funding solution, the actual cost is higher for people with the purpose of buying a car than a loan.

And the auto financing leasing industry often has continuous disputes. Some auto financial leasing platforms only highlight the "low down payment" but do not emphasize that car ownership is not in the hands of customers who are usually not familiar with auto financing leasing. Some consumers have signed the contract without knowing specific matters, but the core issues are not clarified, with some troubles to be settled.

From the corporate perspective, the current credit investigation system is not sound, the used car evaluation system and the circulation system are not mature enough. Auto financing leasing companies need to invest resources in risk control, and they have to face the possibility of losses when handling second-hand cars. These are objectively Enterprises have increased costs.

Moreover, the low threshold model of auto financing leasing is easy to be targeted by black households. As the domestic auto financing leasing industry is still in its infancy, information between companies is not interoperable. Some companies only review basic information such as driver's licenses, ID cards, and credit cards when signing a contract, and their risk control capabilities are insufficient. In addition to the information review before the lease, there are also risks during and after the lease.

Although there are many shortcomings in the development of automobile financial leasing at this stage, the market value of automobile financial leasing which is a new model with both advantages and disadvantages for the domestic auto trading market cannot be ignored. Only when enterprises and consumers abide by market rules and fully respect the wishes of both parties can the industry develop well.

Custom Reporting

https://www.globalmarketmonitor.com/request.php?type=9&rid=0

We provide more professional and intelligent market reports to complement your business decisions.

Chinese

Chinese