Photovoltaic auxiliary materials occupy an important position in the production of photovoltaic modules. Photovoltaic modules are mainly composed of glass, plastic film, solar cells, backplane, aluminum frame, junction box, soldering tape, silica gel, and packaging materials. Among them, the production of solar cells has gone through the links from silicon materials to silicon wafers to solar cells. These three links have played a decisive role in the process of the photovoltaic industry from laboratory to commercialization, which is conducive to the current vigorous development of the photovoltaic industry. However, it cannot be ignored that other materials (usually referred to as auxiliary materials), except for the solar cells, also occupy a considerable position as there are relatively few technological changes and the small cost reduction in auxiliary materials. The position of the auxiliary materials in the component is constantly improving.

Auxiliary Materials Expansion Cycle Is Long, Which Has Multiple Barriers

The unit investment cost of the new production capacity of auxiliary materials has a relatively small decline and the expansion period is longer. The decrease in the unit investment cost of the new production capacity can drive the decrease in the unit depreciation cost. In the past, all the links of silicon material-silicon wafer-cell-component (except auxiliary materials) realize the cost reduction by equipment localization, technological transformation, and large-scale production, especially in the areas of silicon and solar cells. However, due to the small changes in the equipment and technology used for auxiliary materials, the unit investment in new expansion capacity has not significantly decreased in the past few years. And for the expansion of auxiliary materials, it generally takes a long time period, especially for photovoltaic glass. Once it is put into production, it is not easy to stop production, so manufacturers are more cautious about investment.

The auxiliary materials industry has multiple barriers that hinder the entry of new participants, including technology, customer resources, and product certification, and financial barriers. For one thing, products need to pass professional certification to be recognized by manufacturers as photovoltaic modules have strict requirements for packaging materials, which requires investing a lot of cost of the professional equipment and follow-up R&D. For another thing, they between suppliers and consumers generally establish long-term and stable cooperative relations as the supplier selection process of photovoltaic module manufacturers is complicated, which constitutes a certain barrier to customer resources for new manufacturers.

Global PV Demand: It Ushered in a Recovery in the Second Quarter of 2020, with a Large Medium and Long-Term Demand Space

In 2020, the photovoltaic market in China ushers in the last year of subsidies. Although the beginning of the year is affected by the epidemic, the Q1 policy has been implemented in advance. The certainty of bidding and household growth is strong, which can offset the epidemic’s impact on photovoltaic installations. Looking at the whole year, the new photovoltaic installed capacity in China is expected to reach 40-45GW in 2020.

Overseas photovoltaic demand is expected to gradually recover. The global photovoltaic market demand has basically been affected by the epidemic. At present, most economically developed markets have passed the stage of a high incidence of confirmed cases and are gradually liberalizing economic activities. It is expected that new photovoltaic demand will restore in the third quarter.

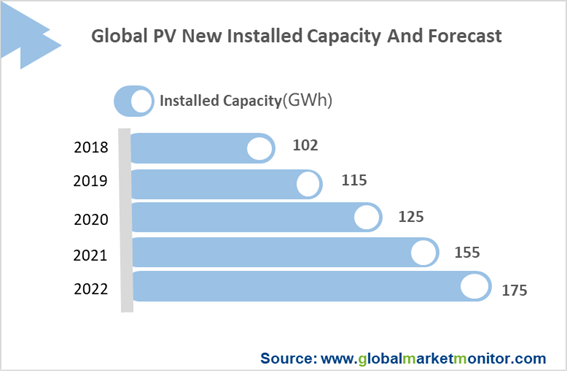

In the first quarter of 2020, the module export volume of China reached 14.76GW. In 2019, module prices in overseas markets fell by 20% throughout the year, which has exceeded the historical average drop and enough to stimulate global demand. However, considering the impact of the epidemic, it is expected that the annual new installed capacity in overseas markets will reach 80-90GW. It is estimated that the global PV installed capacity will be 125GW in 2020, an increase of 9% year-on-year, and the global market will return to high growth in 2021, with an estimated installed capacity of 155GW, an increase of 24%.

The Penetration Rate of Photovoltaics Continues to Rise Under the Trend of Clean Energy and Affordable Photovoltaics

It is estimated that the theoretical penetration rate of photovoltaic power generation in various countries in 2019 was only 3.0%, and the EU reached 4.9%. The penetration rate in many emerging markets is still low, which means that there is still a lot of room for development in the future. Looking forward to the future, the trend of energy electrification is accelerating and the cost of photovoltaic power generation in the era of parity is gradually reduced, and energy storage is rapidly introduced, causing that the proportion of incremental photovoltaic power generation is gradually increasing. At the same time, the coverage of photovoltaics will also be wider, which will break the situation where the PV demand depends on a few large markets.

The Adhesive Film Is A Key Material for Photovoltaic Auxiliary Materials, And the Market Demand Is Increasing Steadily

Adhesive film is a module packaging material, placed between the module's tempered glass or backplane and the solar cell to encapsulate and protect the cell, mainly including EVA film and POE film, in which nearly 90% of the production cost comes from EVA resin.

Enquire before purchasing this report-

https://www.globalmarketmonitor.com/request.php?type=3&rid=589445

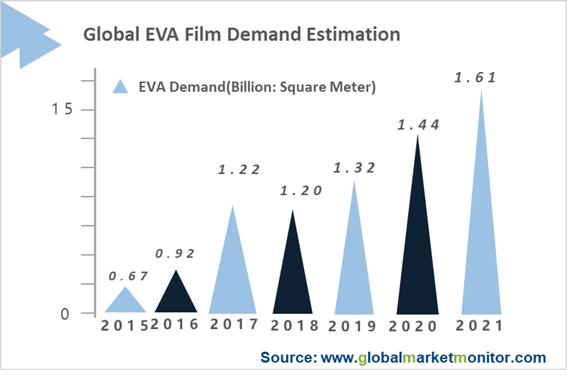

With the continuous increase of global photovoltaic installations each year, the demand for EVA films from module manufacturers is also increasing. It is expected that the global demand for EVA films from 2019 to 2021 will reach 13.2, 14.4, and 1.61 billion square meters, respectively.

EVA Film Has Been Replaced by Localization, And the Market Pattern Is Stable

The film production process is relatively mature, and the gross profit margin of leading companies is maintained at about 20%, mainly from the cost advantage built by the scale effect.

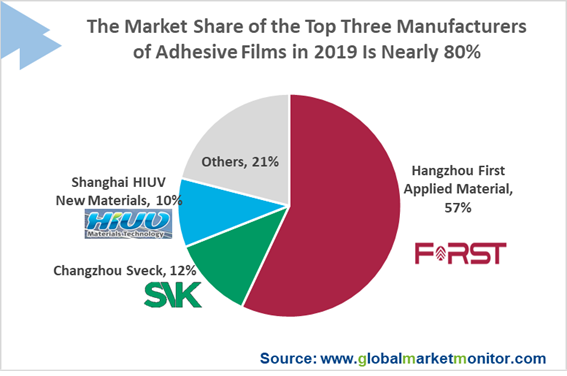

At present, the pattern of the film sector is stable, and Hangzhou First Applied Material's leading position is sound. EVA film is highly professional in terms of formula, modification technology, and production technology, and key production equipment, which has strict requirements on product transmittance, shrinkage, and aging resistance. Thus, it takes many years of exploration and continuous improvement to ensure product quality. Before Foster's large-scale production of EVA film, the global market was dominated by four companies, of STR in the United States, Mitsui Chemicals Fabro in Japan, and Bridgestone in Japan, and Etimex in Germany, whose total market share reached more than 60% in 2013. Due to the rapid growth of the photovoltaic module output of China, the demand for EVA film is also growing.

In 2007, under the situation that China had the world's largest demander of EVA film, early domestic companies that invested in the research and development of EVA film through independent research and development or technical cooperation have gradually realized the localization of EVA film. After solving the problems of anti-aging and light transmittance of EVA film, they gradually began to occupy the market.

Enquire before purchasing this report-

https://www.globalmarketmonitor.com/request.php?type=3&rid=166877

After 2011, Changzhou Sveck and Shanghai HIUV gradually squeezed the market share of foreign companies.

In 2019, the localization rate of EVA film has exceeded 80%, and Hangzhou First Applied Material has even occupied half of the global photovoltaic film market.

The adhesive film which has a high degree of importance accounts for a low proportion of component cost, with a low sensitivity to price. Taking monocrystalline PERC photovoltaic modules as an example, EVA film accounts for a relatively low proportion of module cost, only about 4%. Module manufacturers are not sensitive to the price of EVA film, but have high-quality requirements. The industry concentration is expected in the future Will be further improved.

LEARN MORE:

EVA Film for Solar Cells

https://www.globalmarketmonitor.com/reports/166877-eva-film-for-solar-cells-market-report-2019.html

EVA Resin

https://www.globalmarketmonitor.com/reports/589445-eva-resin-market-report.html

Solar Photovoltaic

https://www.globalmarketmonitor.com/reports/406047-solar-photovoltaic-market-report.html

We provide more professional and intelligent market reports to complement your business decisions.

Chinese

Chinese