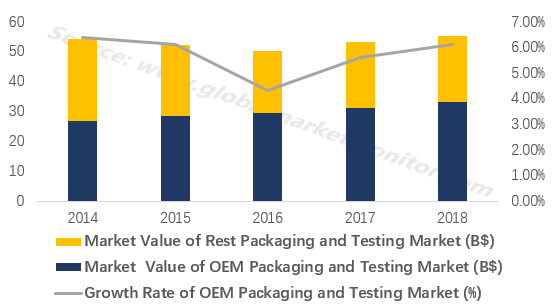

With the upgrading of the semiconductor industry, all links in the industrial chain have gradually become specialized. At present, global market value of OEM (Original Equipment Manufacturer) packaging and testing market has exceeded 30 billion dollars, accounting for about 60% of the global packaging and testing market. Due to the labor-intensive nature of the packaging and testing process, the market share of OEM packaging and testing is likely to be bigger, and Chinese OEM packaging and testing enterprises will catch up with the leading enterprises.

OEM packaging and testing market is growing

![]()

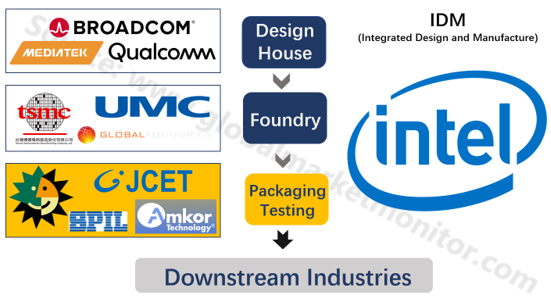

Unlike those IDM (Integrated Design and Manufacture) enterprises, most semiconductor enterprises are taking ‘Design House-Foundry-OEM Packaging and Testing’ model. OEM production is actually a division of labor to refine competition, which not only conduct enterprises to "do what they are best at", but also optimize the resource allocation of the entire semiconductor industry chain. Also, buy the service of packaging and testing from OEM enterprise in developing countries and regions is helpful to reduce cost and takes advantage from a lower product price.

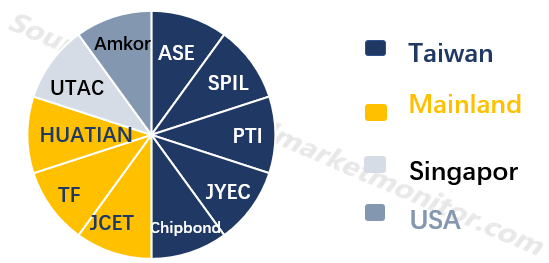

Most leading OEM packaging & testing manufacturers are in Asia

![]()

China Taiwan is the most influential region in OEM packaging and testing market. Since 2014, Taiwan has always been TOP1 with the market share of around 50%. According to the location of the headquarters, 5 of the TOP 10 in 2018 come from Taiwan. And mainland China is catching up through acquisitions and mergers, with 3 enterprises in the TOP 10.

As for countries and regions like America, Europe, Japan, Singapore and South Korea, they have fewer OEM packaging and testing enterprises. Among the TOP 10 in 2018, only America and Singapore have a share, with one enterprise on the list for each. However, these countries and regions have strong IDM companies with internal packaging and testing departments.

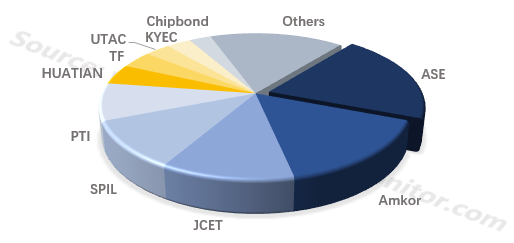

Most TOP 10 are Taiwan OEM packaging & testing manufacturers

![]()

In recent years, the semiconductor industry has entered a mature stage, and the competition has become fiercer. Manufacturers have expanded their scale through mergers and acquisitions or made strategic layouts for the future, and the concentration of the industry is growing. And this is the same in OEM packaging and testing market.

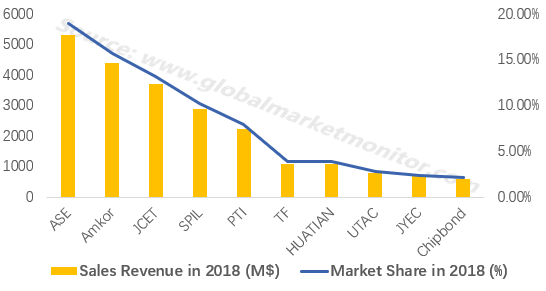

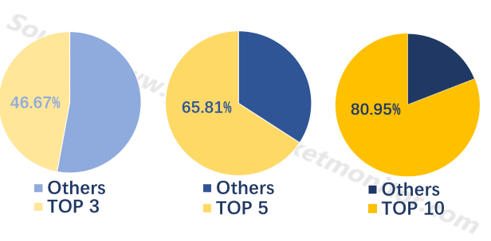

Top 10 take 80.95% of the OEM packaging & testing market

![]()

OEM packaging & testing market is highly concentrated

![]()

In fact, the semiconductor packaging and testing industry is more concentrated than it seems. In 2017, ASE who ranked the first acquired SPIL’s equity. And Ankor who ranked the second first acquired the equity of J-Device in 2016, and then Nanium in 2017. In September 2018, HUATIAN and its controlling shareholder TSHT jointly acquired 75.72% of the total outstanding shares of Malaysian packaging and testing company Unisem (M) Berhad, of which HUATIAN acquired 60%.

Through acquisitions and mergers, those leading companies have far more control over the market than their own market share. Cases of existing small and medium-sized companies being acquired or merged are countless, and it is extremely difficult for new entry enterprises to survive in the packaging and testing industry. Among all the OEM packaging and testing companies, Taiwan's ASE has been TOP 1 for many years.

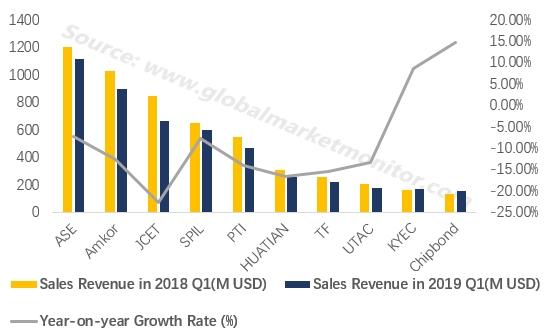

ASE still takes the biggest part in 2019Q1

![]()

However, as the global semiconductor industry continues facing challenges in 2019, the packaging & testing industry has also been affected.

Only KYEC and Chipbond remain increasing

![]()

The impact of this shock is directly reflected in the performance of the first quarter of 2019. The enterprises on the list of the TOP 10 has changed, and only two of them have maintained positive revenue growth. ASE is not on the positive growth list, and there are even rumors about UTAC biding for the sale of 1 billion USD after its layoffs.

KYEC and Chipbond, whose revenue are growing, one benefited from the early plan on 5G,the other owe its customer—Boe. Other semiconductor packaging and testing companies should learn from the two to survive the current downturn.

KYEC maintains close contact with its customers and provides real-time test assistance to meet customer needs. Its cooperation with Qualcomm, except for renting a dust-free factory, also targeting on 5G chip development and testing projects. The continues investment on joint research and development projects drove its revenue growth of 8.6% in the first quarter of 2019, and the revenue in the rest of the year is also expected.

Chipbond benefited from its customers, panel maker BOE, as latter’s demand increased. And the first quarter revenue increased by 14.7%. In the future, under the continuous full capacity of BOE's panel production, Chipbond's annual revenue performance will be satisfactory.

We provide more professional and intelligent market reports to complement your business decisions.

Chinese

Chinese