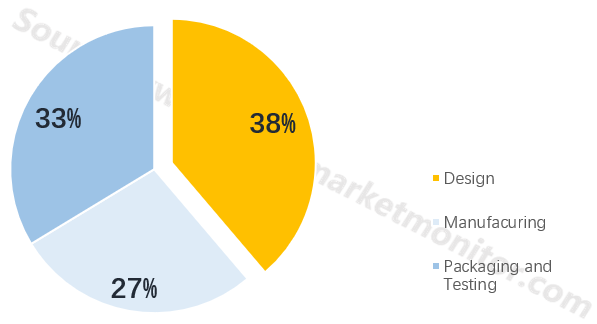

In semiconductor industry, IC design is the most important sub-sector, which determines the current status and also guides the development direction. Currently, the IC design industry accounts for 38% of the entire semiconductor industry. As technology advances and production costs decline further, the proportion of the IC design industry will increase.

IC design is the most profitable Semiconductor segment

![]()

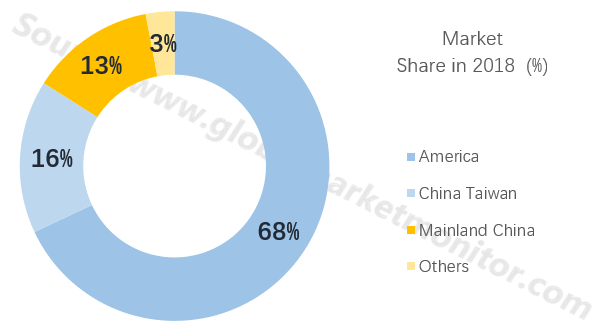

Based on the principle of maximizing profit, the other two sub-sectors of the semiconductor industry—manufacturing and packaging & testing—have moved to Asia Pacific region. The design industry, which is the upstream of the entire semiconductor industry, is a knowledge-intensive industry and is still dominated by US companies. The semiconductor design industry has high technical barriers. American companies have developed for a long time and have abundant human resources, and other regions are far behind America on design techniques.

America is still dominating IC design market

![]()

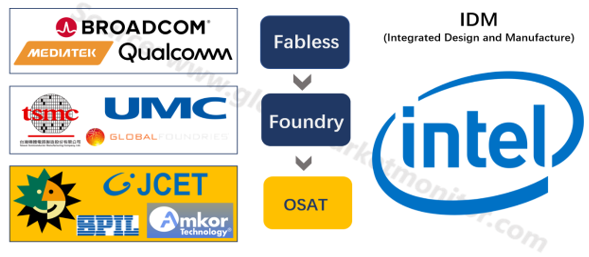

Although the transfer of the design industry is not obvious, it has also undergone significant changes, and finally formed the status quo of the current two camps. One is the Integrated Device Manufacturing (IDM) model, whose representatives are Intel and Samsung. The other is the “design-manufacture-package-testing” model led by Fabless, and representative Fabless are Qualcomm and Broadcom.

Both IDM and Fabless have influential enterprises

![]()

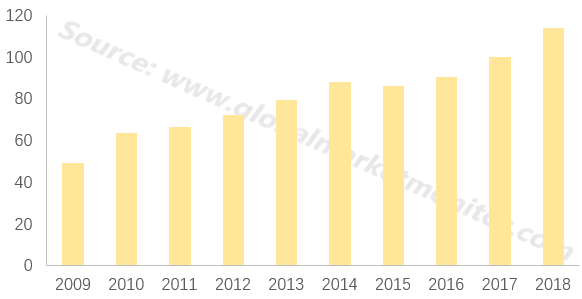

Fabless optimizes industry resource allocation and overall turnover is on the rise. In 2018, global sales revenue of fabless industry reached 113.9 billion dollars, and the compound average growth rate (CAGR) since 2009 was 9.75%. Compared with the 100 billion US dollars in 2017, it was up 13.9% year-on-year.

The business operations of Fabless are more flexible than IDM, but Fabless has no production lines and needs to rely on orders from downstream application companies. If Fabless' partners are too single, it will be highly vulnerable to customers and may even face a crisis due to the loss of customers.

Sales Revenue of fabless industry grows with a CAGR of 9.75%

![]()

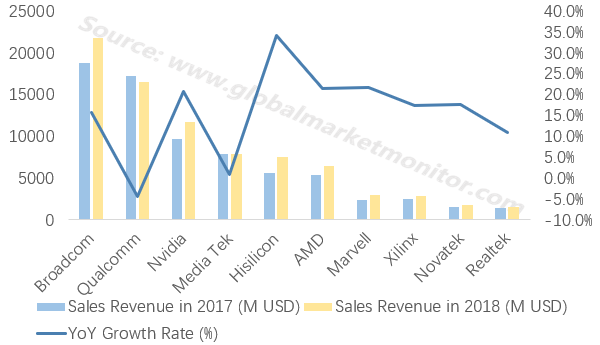

At present, Fabless industry is relatively concentrated. The top ten Fabless have a total revenue of $81 billion US dollars in 2018, accounting for 71% of the total global revenue. Compared with the total revenue of $72 billion in 2017, the total revenue of the top 10 Fabless increased by 12%. The only company with negative growth was Qualcomm. Its total revenues decreased $762 million, a decline of 4.4%.

Only Qualcomm suffered a decrease in 2018

![]()

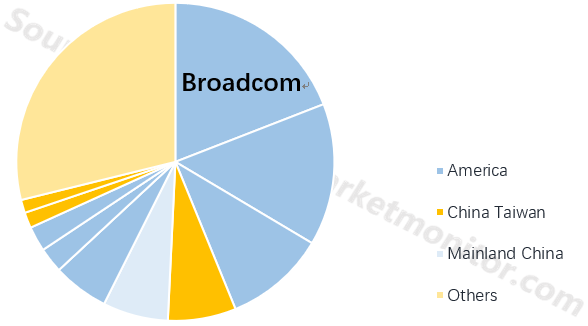

Of the top 10 Fabless, six are from the United States, accounting for about 55% of total revenue in 2018. Among them, Broadcom accounted for 19.1% of the total global revenue.

![]()

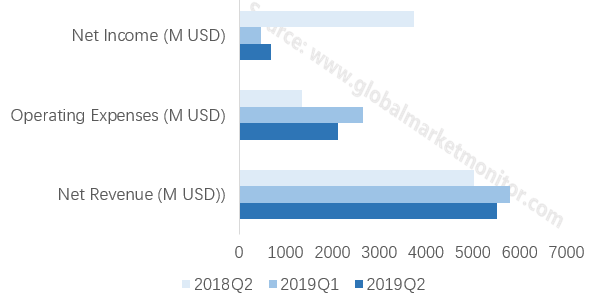

Broadcom's revenue for the second quarter of 2019 increased 10% year-on-year and 4.7% quarter-on-quarter. Gross profit margin for the second quarter was 56%, higher than the 55.4% in the first quarter and 50.9% in the same period last year. Operating expenses were $21.9 billion, an increase of $769 million year-on-year, but net profit was $691 million, a decrease of $3 billion year-on-year.

![]()

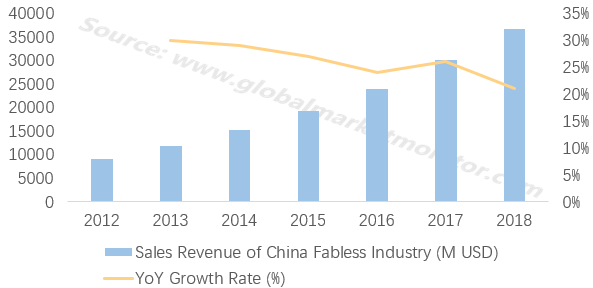

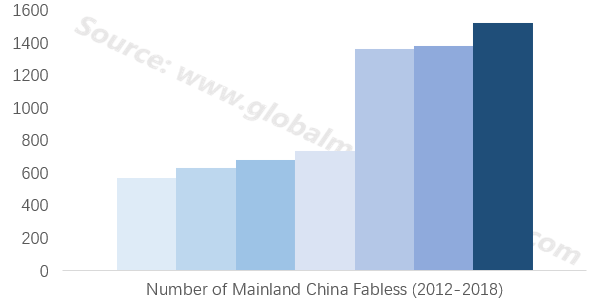

Hisilicon has the largest increase among top 10 Fabless, and the increase is up 34.2% year-on-year. This is consistent with the general environment of the Chinese semiconductor industry. In 2018, the revenue of China's IC design industry reached US$36.6 billion, an increase of nearly 23% annually. Hisilicon is backed by Huawei Group and has a reliable downstream market. It is ahead of other Chinese mainland Fabless, and what followed are UNISOC and Beijing Haowei.

The growth of Fabless in mainland China might slow down in 2019

![]()

![]()

However, demand for consumer electronics declined in 2019 and the global economic growth slowed. China's IC design industry will slow down in 2019, with an expected revenue of no more than $43.6 billion.

We provide more professional and intelligent market reports to complement your business decisions.

Chinese

Chinese