Due to the increased trade friction between Japan and South Korea, Japan announced on July 1st that sanctions will be applied on the export towards South Korea, including high-purity hydrogen fluoride “used in semiconductor manufacturing”, photoresist “coated on semiconductor substrates” and fluorinated polyamides “for making TV and smartphone display panels”. The restraining order was implemented on July 4th.

This restriction extends the export process of Japanese materials to South Korea, and the process of separately applying for product export licenses takes about 90 days. However, the inventories of semiconductor materials in South Korean companies such as Samsung and SK Hynix are generally 1-2 months. If Japan's sanctions towards South Korea continue to be strictly enforced, South Korean companies will face the risk of supply shortage.

It is reported that South Korean companies are trying to increase purchases from suppliers in mainland China or China Taiwan, and have begun to accelerate testing of companies from mainland China to compensate for the shortage of raw materials as soon as possible. This test usually takes a period of 40-50 days.

Photoresist

Photoresist is a barrier material used in manufacturing to obtain a target pattern structure, and it is a key material for selective etching in a semiconductor lithography process. Due to the extremely high industry barriers, the photoresist industry is in an oligopolistic pattern.

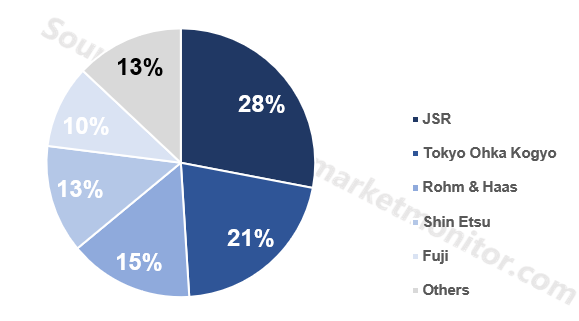

The top five manufacturers account for 87% of the global photoresist market, and the industry concentration is high. Among them, Japan's JSR, Tokyo Ohka Kogyo, Shin-Etsu and Fuji take 72% of the global market share. Among the top five vendors, only Rohm & Haas is a non-Japanese company.

Photoresist market is dominated by Japanese enterprises

![]()

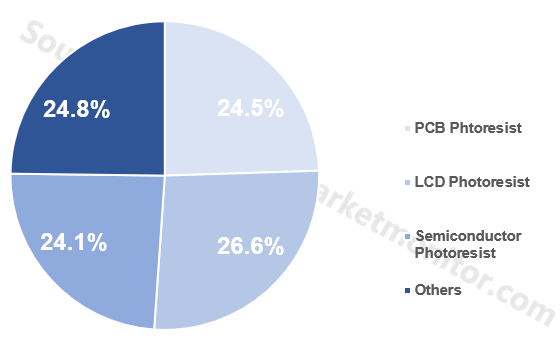

The global downstream applications of photoresists are relatively balanced, with PCBs, LCDs, semiconductor photoresists and other components each accounting for around 25%.

The market shares of photoresist’s applications are even

![]()

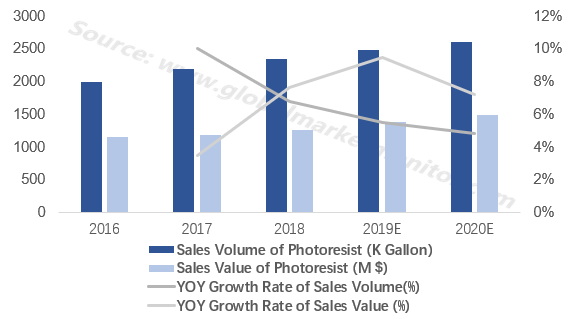

In 2017, global photoresist consumption exceeded 8 billion USD, of which semiconductor photoresist was approximately 1.3 billion USD. The demand for semiconductor photoresists has increased by about 7%-8% per year since 2016. Although the sales growth of semiconductor photoresists has slowed down in recent years, the market scale of semiconductor photoresist market is still accelerating. At present, mainland China is the largest market for semiconductor photoresists.

Semiconductor photoresist market is increasing

![]()

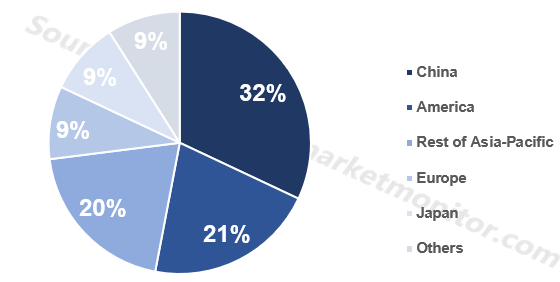

Asia-Pacific market of semiconductor photoresist is huge

![]()

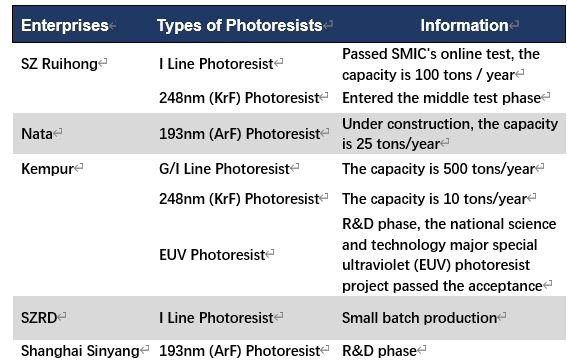

Semiconductor photoresist is the most high-end component of photoresist. The core technology of photoresist in the semiconductor industry is mainly monopolized by Japanese and American companies. The market share of local enterprises in mainland China is extremely low. At present, there are only five semiconductor photoresist production and R&D companies in mainland China, namely Suzhou Ruihong, Beijing Kempur, NATA, and SZRD.

The capacity of Chinese enterprises is small

Considering about the quantity and quality, photoresist of China and other regions cannot replace Japanese photoresist, and South Korean companies still need to rely on Japanese companies in a short term. Therefore, Japan’s sanctions against South Korea are expected to greatly influence Korean wafer fabs and related companies. In the absence of raw materials, South Korean companies are very likely to guarantee the production of high-end products by reducing the production of low-end products. Under this circumstance, companies in mainland China and other regions will have access to a market which has monopolized by Japanese companies.

China's semiconductor photoresist is still in its infancy and its output is low. However, most of the semiconductor photoresist companies in mainland China undertake major national science and technology projects, and they have the support of national talent resources in scientific research and have good development prospects. Although it is unlikely that these semiconductor photoresist companies will expand their market share in this Japan-Korea friction, this friction has made the world see the necessity of independent controllability of the supply chain, which will greatly promote Chinese semiconductor photoresist industry. In addition, mainland China is the largest market for semiconductor photoresist, which is a favorable support for the development of local photoresist companies.

High-purity hydrofluoric acid

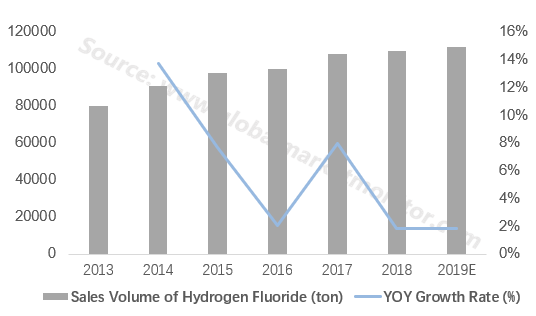

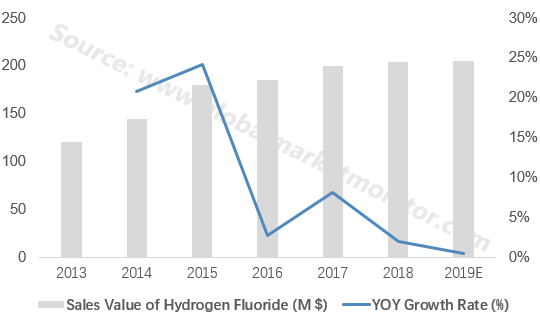

High-purity hydrofluoric acid is mainly used for wafer surface cleaning, chip cleaning and corrosion, and is one of the key auxiliary materials in the integrated circuit industry. In 2019, global sales of high-purity hydrofluoric acid are expected to be 112,000 tons, and the sales value is expected to exceed 200 million US dollars.

A slowdown in hydrogen fluoride market

![]()

![]()

In the global high-purity hydrofluoric acid market, Japanese companies are in an absolute dominant position. The three leading companies are all from Japan, sharing the market share of more than 93%. Among them, Stella Chemifa accounted for about 63%, Daikin accounted for about 21%, and Morita Chemical accounted for about 9%.

Japan’s restrictions on exports of high-purity hydrofluoric acid to South Korea will have a certain impact on South Korea’s semiconductor industry and other industries related to high-purity hydrofluoric acid, while South Korean domestic companies cannot fill the vacancy of high-purity hydrofluoric acid, seeking other external suppliers becomes South Korean companies’ inevitable choice.

Due to the impact of economic globalization, South Korean companies are likely to ease the shortage of raw materials by working with overseas factories of Japanese companies. Stella Chemifa's high-purity hydrogen fluoride plants in South Korea and Singapore all have the ability to supply South Korean companies. And from a legal perspective, Japanese companies can continue to work with South Korean companies through overseas factories.

If the cooperation between Japanese companies' overseas factories and South Korean companies is not restricted, Japan's raw material sanctions against South Korea may be greatly reduced, and companies in other regions may also weaken their market share. However, this must be based on the expansion of overseas factories in Japan. The existing production of Japanese overseas factories is consistent with the original orders, and it is generally not possible to give priority to South Korean companies.

Mainland China is rich in hydrofluoric acid production capacity, with a total annual output of more than 1.65 million tons, and it is a net exporter of hydrofluoric acid. However, the production of high-purity hydrofluoric acid in mainland China accounts for only 5% of the domestic demand and still depends on imports.

At present, Zhejiang Sanmei, DFD, Juhua, Jingrui and other companies in mainland China have the ability to produce high-purity hydrofluoric acid. It is expected that these companies will benefit from the partial transfer of orders from Japan's export restrictions. DFD clearly indicates that its semiconductor hydrofluoric acid has reached the UPSSS level and can replace Japan's products. Many South Korean companies have come to negotiate with DFD, and a good growth in export is expected.

The Japanese sanctions against South Korea on the one hand inspired the Chinese government to promote the independent controllability of the supply chain, on the other hand stimulated enterprises to develop high-purity hydrofluoric acid products. Even if some companies miss the opportunity to enter the South Korean market, there is a huge Chinese market to be the backing of local companies. And a major upgrade of China's related industries is likely to happen.

Fluorinated polyimide

Polyimide has the advantages of high temperature resistance, high insulation, high stability, excellent mechanical properties, etc. It can be widely used in flexible displays, flat panel displays (FPD), flexible solar cells, semiconductor devices and other fields. Fluorinated polyimide is a kind of polyimide, and is mainly used in flexible screen substrates and folded OLED covers.

More than 90% of the world's fluorinated polyimides come from Japanese suppliers such as Sumitomo Chemical, Shin-Etsu and JSR. Although South Korea's domestic PI film supplier SKC has fluorinated polyimide production capacity, South Korean companies still face the problem of insufficient capacity. Due to the shortage of key materials, the flexible OLED business of panel makers such as Samsung and LG in South Korea is expected to be affected in a short term.

At present, Samsung and LG are still the world's major suppliers of flexible OLEDs, accounting for more than 90% of the global market. However, due to Japanese raw material sanctions, the capacity of South Korean companies cannot be guaranteed in the future. This is a good opportunity for panel makers in mainland China to expand their shares, especially those leading enterprises like BOE, CSOT and Visionox.

The Japanese government’s export restrictions on South Korea are very firm. Even if South Korea appeals to the WTO, the Japanese side has indicated that it will not lift restrictions on South Korea. On July 10th, the Japanese side even indicated that it may implement “additional measures” to sanction South Korea, that is, to put more raw materials into the restriction list or to change “restrictions” to “banned sales”. For such a prospect, South Korean companies can only accelerate the search for alternative products. This is indeed an excellent opportunity for mainland China’s companies to enter the mainstream market, but not every company has the capability to seize the opportunity.

We provide more professional and intelligent market reports to complement your business decisions.

Chinese

Chinese