With the official application of 5G network, both the demand and the price of its upstream product, printed circuit board (PCB) has increased. Affected by this one and only downstream industry, copper clad laminate (CCL) industry will welcome an in-depth revolution.

Traditional CCL market is shrinking

Copper clad laminate (CCL) is the basic material of PCB. Since PCB is the one and only downstream industry of CCL, the end product of CCL is the application of PCB in computer, communication equipment, consumer electronics, automotive electronics and other industries. When used to make multi-layers PCB, CCL is also called core board (CORE), which is responsible for the function of conduction, insulation and support.

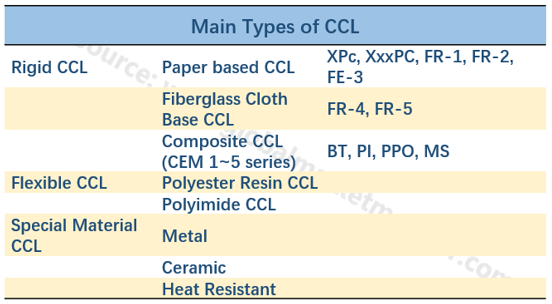

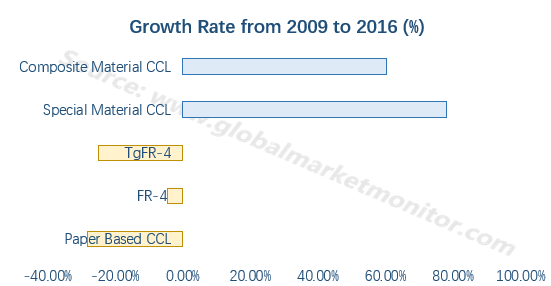

CCL can be divided into three categories based on the differences of structure: rigid CCL, flexible CCL and special material CCL. At present, traditional epoxy fiberglass substrate CCL is most wildly used, especially type FR-4. But traditional CCL market is already mature and in the danger of shrinking. What following is the rapid development stage of combined CCL and special CCL.

The market of traditional CCL is shrinking

Manufacturers of mainland China dominate the low-end market of CCL

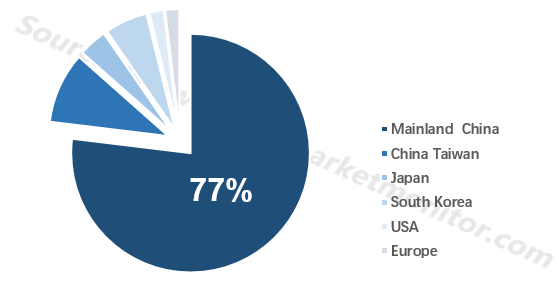

From 2011 to 2016, the global market value of CCL increased from 9.5 billion USD to 10.1 billion USD. During these five years, Chinese CCL companies continued to expand their domestic and international markets and gradually occupied the low-end market of CCL. And its market share of CCL in the world increased from 59% to 65%.

In terms of production, as China's CCL production capacity is concentrated in the low-end market, its global share of CCL production far exceeded its global share of value, reaching more than 77% of global production.

Most CCL were made in mainland China

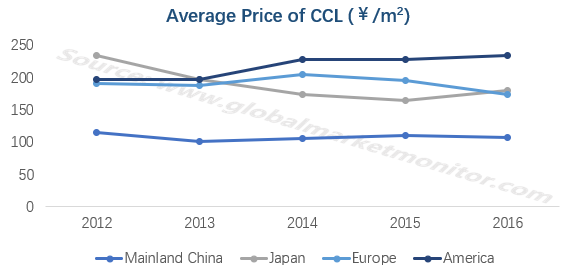

CCL of mainland China is much cheaper than that of others

Although the middle and low-end market of CCL will shrink under the pressure of special material CCL, but cyclical boom will continue. And there are several reasons for it.

First, the rise in the price of upstream raw materials, which accounts for a very high proportion of the traditional CCL operating costs, may push up the price of CCL.

Second, the oligopoly effect gradually emerges, leading companies in CCL industry will gradually obtain the ability to control the production and the price of CCL market.

Also, as environmental supervision becomes more stringent, a large number of unqualified manufacturers will be shut down. And environmental inspection is expected to become a routine, the production of CCL will be controlled and periodically out of stock might happen.

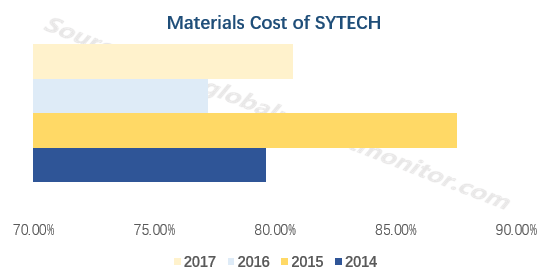

Materials account for an absolute majority of manufacturing costs

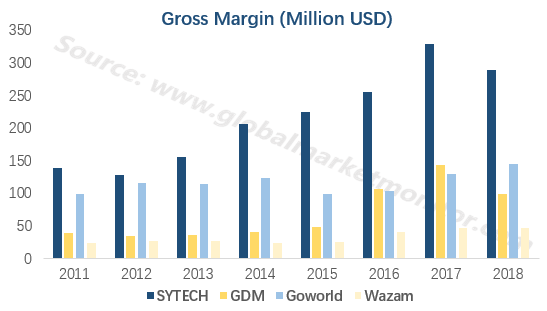

Mainland China’s CCL leading manufacturers are profitable

High profit and barrier of special material CCL

Special copper clad laminates are usually customized by downstream PCB processing faucets and PCB downstream equipment manufacturers according to their own needs. Product parameters vary, and the average unit price and market size are difficult to estimate.

In addition, customized special copper clad laminates are not universal, and most of them have the characteristics of small batch size and high added value, and are usually used in the flagship products of downstream manufacturers. The high-tech features of the downstream flagship products further enhance the technical threshold of special copper clad laminates.

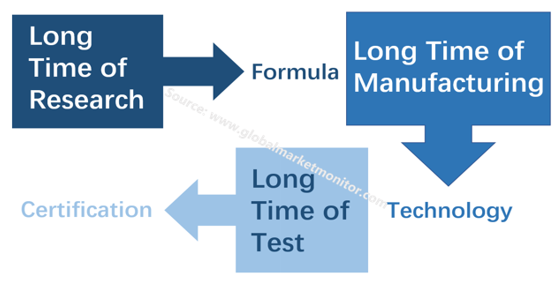

It takes a long time to have certification and the trust of clients

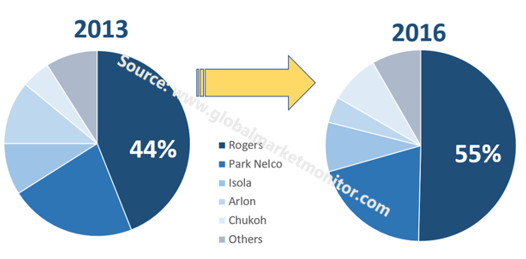

Among all the manufactures of special material CCL, Rogers is a well-deserved benchmark. As early as the 1950s, Rogers already produced military-grade PTFT. And in 1970s, Rogers’s civilian series products were introduced. The advanced layout allowed Rogers to complete the accumulation ahead of time, and became the first to cross the high barrier of special material CCL.

While Rogers has enjoyed the benefits of the accumulation, many companies are still working hard to obtain orders from downstream manufacturers, and more low-end companies are still in the research and development stage.

Most of China's CCL companies have not yet achieved special CCL production, but several leading enterprises have already entered the special CCL supply chain. Also, most of China’s CCL manufacturers are already in active research and development. China's special CCL industry is expected to develop.

Rogers is the leader of PTFE-CCL manufacturing

China’s manufactures can rely on communication industry to speed up

Mainland China’s CCL companies have lost their opportunities and are lagging behind by foreign companies in high-end formulas, but they can accelerate their development by cooperating with the strong downstream communication equipment manufacturers. Rather than buying special material CCL from foreign manufactures with a high price, China's communication equipment manufacturers tend to cultivate their own supply chain ecosystem. This is not only for cost saving, but also for satisfy every need of themselves.

SYTECH is the first mainland CCL manufacture to enter the high-end field by applying introduced formula while carrying independent research. Since SYTECH focuses on CCL business only, it has obtained a good collaborative research and development relationship with related downstream manufactures. At present, SYTECH is already in the supply chain of special material CCL and its development mode has reference significance for other CCL enterprises in China.

We provide more professional and intelligent market reports to complement your business decisions.

Chinese

Chinese