Glass fiber is a kind of inorganic non-metallic materials with excellent performance. It has a wide variety of advantages, including good insulation, strong heat resistance, good corrosion resistance, and high mechanical strength, but the disadvantages are brittleness and poor wear resistance. It is made of six kinds of ores of pyrophyllite, quartz sand, limestone, and dolomite, as raw materials through high-temperature melting, drawing, winding, weaving, with the diameter between a few microns and more than twenty microns, and each strand of fiber strands consists of hundreds or even thousands of monofilaments. Glass fiber is usually used as a reinforcing material in composite materials, electrical insulation materials, thermal insulation materials, circuit boards, and other fields of the national economy.

Enquire before purchasing this report-

https://www.globalmarketmonitor.com/request.php?type=3&rid=370058

The global fiberglass industry, originated from the United States, was born duo to the establishment of the Owens Corning Company in 1938. As conventional materials were scarce after the outbreak of the Second World War, glass fiber was used as an alternative material to meet military combat readiness needs. Subsequently, people discovered that this material has more and more advantages, using it in aircraft, tanks, body armor, and weapons, thus, the glass fiber industry has begun to obtain improve dramatically.

A Big Producer That Grew Up from the Cracks

The development of glass fiber in China began in 1958. Since glass fiber was initially used in the military field, developed countries in Europe and the United States imposed a technical blockade on China for a long time, resulting in a late start and slow development of China’s glass fiber industry. Though sixty-year accumulation, China has always insisted on independent research and development and made great progress.

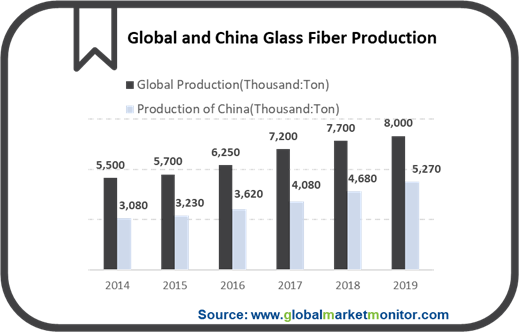

In 2010, the global economic recovery brought high growth in the glass fiber industry, and production capacity has gradually expanded since 2017. In 2018, the global glass fiber production capacity reached 7.7 million tons, which reached 8 million tons at the end of 2019, and the production capacity is concentrated in leading companies.

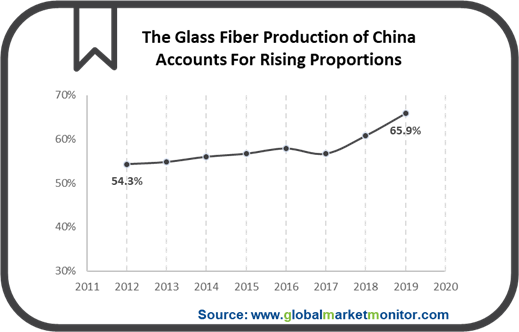

In 2019, the output of glass fiber in mainland China reached 5.27 million tons, accounting for more than half of the total global output. China has become the world's largest glass fiber producer. From 2012 to 2019, the average annual compound growth rate of the glass fiber production capacity reached 7%, which is higher than the global average annual compound growth rate of glass fiber production capacity.

In seven years, the proportion has increased by nearly 12%, which can be seen is that the increase in global glass fiber supply mainly comes from China where the glass fiber industry is expanding rapidly, establishing a leading position in the world glass fiber market.

Market Pattern: High Production Capacity Concentration and Strong Industry Monopoly

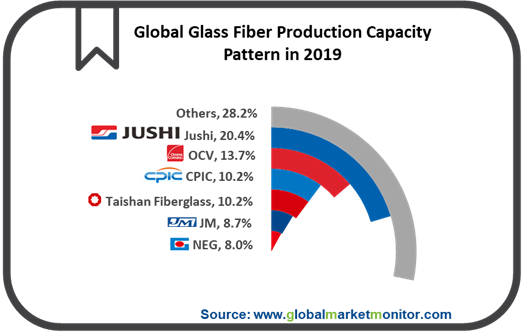

The fiberglass industry is a capital-intensive and technology-intensive industry, with strong industry monopoly. There are six major manufacturers, including Jushi, Taishan Fiberglass, CPIC, OCV, NEG, and Johns Manville, all of which account for more than 70% of the total global glass fiber production capacity.

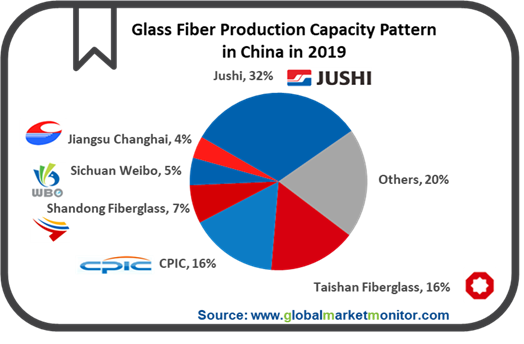

Domestically, Jushi, Taishan Fiberglass, and CPIC are the three giants in the domestic fiberglass industry, with a total market share of 64% of the domestic total production capacity. Together with Shandong Fiberglass, Sichuan Weibo, and Changhai, the total production capacity accounts for 80%.

Under the structure that both the global market and the domestic market have the characteristics of concentrated production capacity, large-scale fiberglass companies have greater competitive advantages. Companies with weaker competitiveness are likely to be gradually squeezed out of the industry and emerging companies is hard to enter the market.

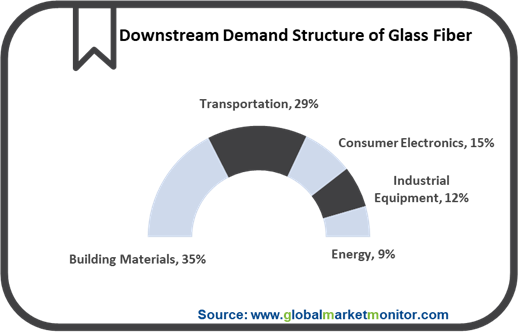

Downstream Demand Multi-Wheel Drive, Glass Fiber Market Is Far from the Ceiling

The downstream market of glass fiber is mainly distributed in building materials, transportation, consumer electronics, industrial equipment, energy.

The continued downward trend in the domestic glass fiber industry in 2019 is due to the rapid deterioration of the relationship between supply and demand, especially the impact of new capacity. The industry's production capacity expanded rapidly from 2017 to 2018, and the original yarn production capacity was increased by 250,000 tons and 900,000 tons respectively in two years. Domestic demand is expected to rebound at the bottom in 2020, mainly due to the increase in wind power installations, the weak recovery of automobile production, and the PCB industry driven by 5G. It is expected that the demand for wind power yarn, thermoplastic yarn, and electronic yarn will further increase and that the building materials and industrial fields will be relatively stable.

Installation Peak of Wind Power Offers the Short-Term Demand

The approaching policy node drives the industry to rush to install on a large scale. With wind curtailment improved, Xinjiang and Gansu are expected to be lifted, and the approved projects in stock will be further released. Since 2019, the phenomenon of wind curtailment has been significantly improved, in which the national average curtailment rate of the first three quarters of last year was 4.2%, a year-on-year decrease of 3.5%. The curtailment rate of Xinjiang and Gansu, which are still in the red restricted construction areas, has improved significantly. As of the first three quarters of last year, the curtailment rate in Xinjiang was 15.4%, a year-on-year decrease of 9.2pcts; the curtailment rate of Gansu was 8.9%, a year-on-year decrease of 10.8pcts. Xinjiang and Gansu are expected to be lifted from the red warnings in 2020. The rush installation has been gradually started in 2019, and 2020 will be an installation peak.

Long-Term Demand Stems from Lightweight Transportation

Global energy and environmental policies have made lightweight traffic a long-term issue for the industry.

The global application of lightweight materials for automobiles is increasing year by year, and there is a large gap between home and the foreign. Germany, the United States, and Japan are currently countries with a relatively high proportion of lightweight materials used in automobiles, among which the application of lightweight materials in Germany accounts for about 25% around world, the highest level. The application level of lightweight materials in domestic automobiles is low, thus, which can be seen that there is large room for improvement.

LEARN MORE:

Glass Fibers

https://www.globalmarketmonitor.com/reports/370058-glass-fibers-market-report.html

E-Glass Fibers

https://www.globalmarketmonitor.com/reports/342466-e-glass-fibers-market-report.html

Custom Reporting

https://www.globalmarketmonitor.com/request.php?type=9&rid=0

We provide more professional and intelligent market reports to complement your business decisions.

Chinese

Chinese